How to Become Financially Independent [Explore Three Steps Inside]

Are you tired of living paycheck to paycheck or feeling trapped in a cycle of debt? Becoming financially independent is a dream for many, but it can be challenging to know where to begin.

In this post, we’ll explore three crucial steps you can take to start your journey toward financial freedom. By implementing these steps, you’ll be well on your way to creating a secure and prosperous financial future.

Table of Contents

What Is Financial Independence?

Everyone has their interpretation of what financial independence means; it can be different for each individual. Let’s look at some of them.

- Some people connect financial independence with managing expenses without external help.

- Many are concerned with retirement savings, striving to balance comfort and current financial obligations.

- For others, the term means you have enough income to last the rest of your life without working despite your age.

Combining all these approaches is critical to achieving financial independence.

Anyone can become financially independent provided they understand what it will take and the discipline and patience to get there. People have gained financial independence with an average salary and a smaller nest egg than you would expect. They’re ordinary people with typical jobs just like yours.

The only real difference is that they were committed to following three key steps.

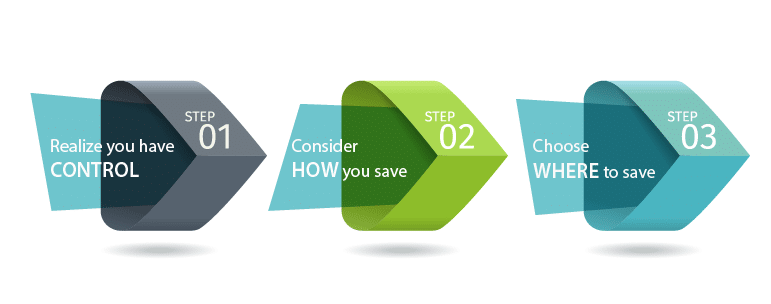

3 Steps to Become Financially Independent

Step 1: Save Money Mindfully

You don’t need a large salary to become financially independent. Some millionaires started off earning the wages of teachers or librarians. So, it’s less important how much you earn and, more importantly, how much you save.

For example,

- John earns $100,000 per year and saves $5,000

- James earns $50,000 and saves $10,000.

James earns less but manages to save twice as much. He builds wealth at a faster rate than John.

Why is it so Hard to Save Money?

We have to combat lifestyle creep. This is when your lifestyle adjusts with increases in discretionary income. Lifestyle creep is dangerous because it results in short-term pleasure that deprives you of saving opportunities. You begin to think it’s your right to spend money on certain things; you deserve it.

If you’re committed to saving money, congratulations. One way to make it easier is to tackle the essential items influencing your savings: house, car, insurance, bank fees or taxes. Reducing your mortgage by $150 may have a more significant effect than saving $5 daily on coffee.

To become financially independent, you must also learn how to save using compound interest and the time value of money (TVM). Let’s define these terms.

What is the Time Value of Money?

The time value of money says the money you have currently is worth more than the same amount in the future. This holds because the funds available now can accumulate interest. The interest generated from the present value makes it worth more today than the same dollar amount in the future. This underscores how important time is as a factor in becoming financially independent.

If you want to save a million dollars in 20 years, you can start saving anytime. However, keeping that money will take much less effort if you start now. That’s because you have the time to maximize another critical saving tool: the power of compound interest.

Understanding Compound Interest

Compound interest means you get extra benefits on the money you saved and the interest you earned. So, investing in a compound interest savings account can make on the initial principal and any accumulated interest over time.

How is Compound Interest tied to the Time Value of Money?

Suppose you have $15,000 and an investment account with a constant 10% interest rate compounded annually. All you want to do is save as much as possible over the next 20 years. The table below shows how much you could earn.

| Time invested | Value at year 20 |

|---|---|

| This year | $100,912.50 |

| 5 years later | $62,658.72 |

| 10 years later | $38,906.14 |

| 15 years later | $24,157.65 |

| 18 years later | $18,150.00 |

| 19 years later | $16,500.00 |

If you have a certain amount in mind, we have a compound interest calculator you can use. If you select Calculate the Opening Balance, you can see what initial investment you need to meet your goal. When you start saving early, you can make much more money than waiting till later.

Learning to save feels like the most challenging part. The desire to spend must be replaced with the need to save.

Step 2: Invest Strategically

You should go further to financial freedom and invest the money you’ve saved. Investing as early as possible is excellent because it gives your money more time to grow. It happens because of the fantastic effect of compound interest.

To become an expert in investing money, our article Compound Interest: Understand It & Use Its Power is a must-read.

Remember! Investments carry some risk, so perform double diligence before committing money to an investment.

Step 3: Generate Passive Income

Passive income is the money generated from an initial effort that takes little or no resources to maintain. You put in the hard work (or money) up front and spend the rest of the time collecting returns.

Generating passive income is more challenging than it sounds; it may take a while to reap the benefits. To do so, you need to invest either money or time (or both) and wait for the dividends from your efforts.

One more critical issue about passive income is taxes. The taxes you pay on passive income may depend on where the money comes from. That’s why it’s essential to keep track of all your earnings.

What are the Best Ways to Get Passive Income?

Several opportunities exist to earn passive income, including

- Rental properties. Generating regular income from rent is a great benefit of owning rental properties.

- Dividend stocks. Investing in dividend-paying stocks can provide regular income without having to sell the stocks.

- Peer-to-peer lending. Investing in peer-to-peer lending platforms can generate interest income.

- Index funds. Investing in index funds is an efficient way to generate passive income, with dividends and capital gains offering a reliable source of financial security.

- Online business. Starting an online business such as a blog, e-commerce store, or affiliate marketing website can provide passive income through advertising revenue or commissions.

- Real estate investment trusts (REITs). Investing in REITs can provide passive income from the rental income generated by commercial properties.

It’s important to note that the best way to earn passive income may vary depending on individual circumstances and financial goals. Having expert advice or conducting thorough research before investing in any venture is essential. With proper consultation, you can be sure about the success of your investments.

The Bottom Line from Financial Freedom Guru

Achieving financial independence requires a long-term plan, discipline to stick with it, and short-term sacrifices. It is possible to become financially independent using the salary of a regular full-time job.

Having read this article, you’ve already taken preliminary actions towards becoming financially independent. Stay with us, and let’s discover the truth about building wealth together.

Last Updated: April 7, 2023