Understanding a Good Credit Utilization Ratio

Updated: July 30, 2022

When reading about credit and credit cards, you may see the term “credit utilization ratio.” If you don’t know what exactly a credit utilization ratio is, the whole discussion can go over your head. Worse, you may be missing out on an easy way to improve your credit score.

Table of Contents

What Is a Credit Utilization Ratio?

Your credit utilization ratio is the amount of revolving credit being used divided by the amount of revolving credit available. Another way to look at it is the amount you owe divided by your credit limit. It’s sometimes referred to as your credit utilization rate.

Imagine you have a total credit limit of $25,000 and owe $5000. Your credit utilization ratio is ($5000 ÷ $25000) x 100%, which equals 20%. You are using 20% of your available credit. Credit utilization ratios can be calculated per card (a per-card ratio) or for all your credit lines.

Utilization ratios are based on revolving credit (credit cards and lines of credit) only. They do not consider installment loans, like a car or mortgage loan.

How Does It Affect My Credit Score and Credit History?

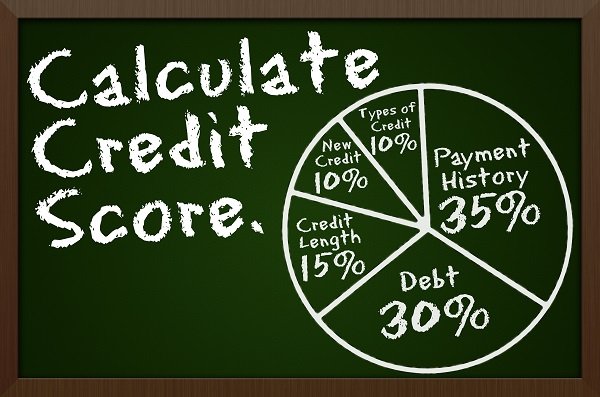

Your credit history and credit score tell lenders if you are a good credit risk. They are determined by credit inquiries (10%), credit mix (10%), average credit age (15%), utilization (30%), and payment history (35%). At 30% by weight, credit utilization is the second largest factor on your credit score.

Utilization tells lenders how you manage credit. A low ratio indicates to lenders that you are controlling your spending wisely, and likely to make sound financial decisions. Conversely, a high utilization warns lenders that you may be overspending and are unable to deal with your financial obligations. Lenders may be worried that if they offer you credit, you would have a difficult time paying them back. If you don’t pay them back, they lose money. All other things equal, a higher utilization will result in a worse credit score than a lower ratio.

What Is a Good Ratio to Have?

Your lender sends your account information to the credit bureaus every month. If your utilization sent to the bureaus is high, then the utilization used to calculate your credit score is high. It’s best to keep your credit utilization at 30% or less. In fact, the lower your utilization is, the better it will reflect in your credit score. You need to make sure to lower the balance on your card by the time your billing cycle ends. (This is your statement closing date.)

Unfortunately, banks sometimes lower your credit limit. You need to ensure your credit used is reduced proportionally. A decrease in your credit limit without a decrease in credit being used will cause utilization to increase. If your $25,000 credit limit from earlier gets reduced by 20% to $20,000, your credit used decreases by 20%. You should reduce your credit usage by 20% of $10,000 (that is, $2000), making your new credit usage $8,000. Your utilization is calculated as $8,000 ÷ $20,000 = 20%.

How to Keep Credit Utilization Ratio Low?

If your credit utilization ratio is high, this is a problem that can be corrected.

- Completely pay off your balance every month and track credit usage on each card. If you can’t bring it to zero, then aim to get it as low as possible. This frees up credit and decreases your utilization ratio. If you don’t think you’ll do a good job monitoring your accounts, automate the monitoring. Set up balance alerts that let you know when you’re nearing 30% usage.

- Make mid-cycle payments. It will help relieve the stress of paying a large bill all at once and work to keep your utilization under 30%.

- Maintain credit cards with zero balances, even if you don’t plan to use them.

- Ask your lender for a credit card limit or line of credit increase.

- Open a new credit card or line of credit. Note that opening a new account will cause your score to drop temporarily. This is because it affects another credit card factor: (new) credit inquiries. Too many inquiries will have a negative effect on your score.

Provided you are not adding to the debt, your credit card balance will decrease, and so will your utilization.

Use One of the Strategies

At 30%, your credit card utilization ratio has a huge influence on your credit history and credit score. The lower you keep the balances on your cards, the lower your utilization will be. For the best results, use one of the strategies listed above. You’ll appreciate the effect on your credit history and credit score.